Iron ore prices take a hit on weak demand amid surge in Platts-observed spot activity

Time:Mon, 27 Mar 2023 07:35:32 +0800

keywords :

Lackluster steel demand and mill margin woes saw buying interest take a hit and iron ore prices hampered in 2022, and the volume of spot activity observed by Platts both on the Market on Close assessment process and outside of it reaching a record high.

Amid signs of market recovery in 2023, let’s take a close look at how the spot market fared through 2022.

The Platts 62% Fe IODEX kicked off 2022 at $119.50/dmt Jan. 3 and dipped to $79.50/dmt Oct. 31 before recovering 48% from the trough to close at $117.35/dmt Dec. 30, S&P Global Commodity Insights data showed.

Here, we unpack the key trends in the iron ore market in 2022 across price assessment participation, preferred pricing mechanisms and brand-level market liquidity.

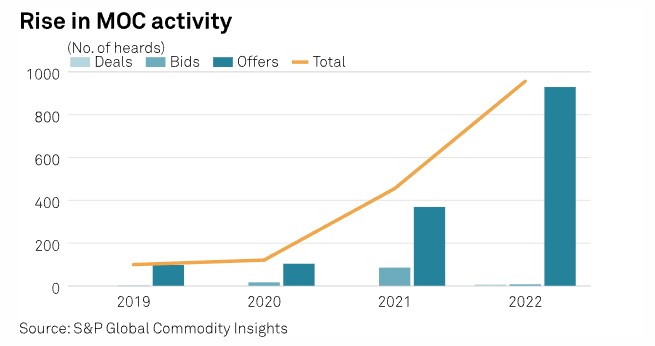

Record high MOC activity

The Platts Market on Close, a structured and highly transparent price assessment process, is used by S&P Global to assess the price of iron ore and other commodities.

Through the MOC process in which bids, offers and transactions are submitted by participants to Platts editors and published in real time throughout the day until market close, our pricing team published a record of 956 lines of iron ore MOC heards in 2022, up 110% from 2021.

Amid weakened iron ore market fundamentals, the MOC process managed to garner more attention and see increased liquidity, particularly offering interest.

The indications reported during the MOC in 2022 totaled 140 offers and three bids, with seven trades concluded.

Growth in trades, pricing points

S&P Global published close to 26,200 lines of iron ore price information, or heards, comprising fines, lump, pellet and concentrates in 2022, up 37% from 2021.

Among the heards, S&P Global observed 1,348 spot transactions for seaborne iron ore, up 39.1% from 2021. Fines accounted for 78.5% of the observed Asian spot trades in the year, followed by lump at 15.2%, pellet at around 5.7% and concentrate at just short of 0.4%.

The volume of spot seaborne iron ore trades S&P Global observed – which may not be all – rose 41% year on year to over 167 million mt in 2022.

In 2022, 57% of the trades observed by S&P Global were collected by our pricing team upon verification from multiple market sources. The balance was directly reported by producers to S&P Global, deals concluded on platforms and in the MOC.

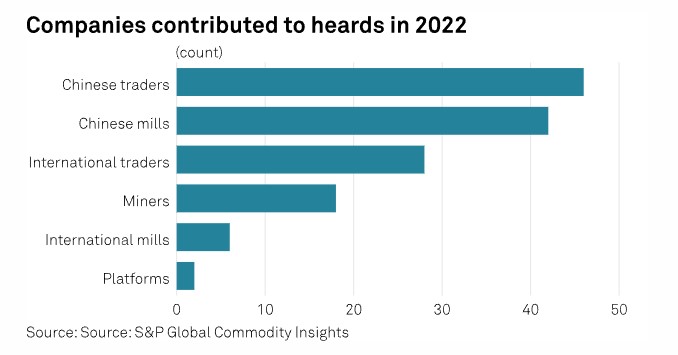

S&P Global also took steps to continue nurturing ties with existing industry sources, with 42 Chinese steel mills, 6 international steel mills, 46 Chinese traders, 28 international traders, 18 mining companies and two platforms having contributed to the price reporting process.

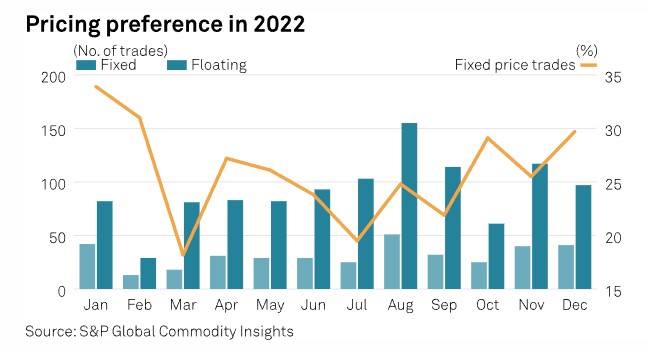

Fixed-price trade revival

The percentage of transactions done on a fixed-price basis was rangebound for most of 2022, regaining momentum among buyers only toward year-end when speculative buying interest surfaced as iron ore prices showed signs of bottoming out and rebounding.

The Platts IODEX plummeted from $147.25/dmt June 7 to $79.50/dmt Oct. 31 before embarking on a road to recovery.

Around 25% of the trades were done on a fixed-price basis in 2022, a tad lower than 26% in 2021, while the other 75% of the trades that S&P Global observed were done on a floating basis, which is index-linked.

Liquidity changes

Aside from supply tightness across the board around February that pushed up the Platts IODEX, overall spot transactions from producers, excluding strips, for medium-grade iron ore fines with higher-Fe content, namely BHP’s Newman High-Grade Fines (NHGF) and Vale’s Brazilian Blend Fines (BRBF), came in at the lower end in 2022.

S&P Global observed the greatest number of spot sales for Rio Tinto’s Pilbara Blend Fines (PBF), the most widely used sintering fines among Chinese mills, in 2022. The greater number of spot transactions observed for PBF is also attributed to its strong trading liquidity.

This is followed by BHP’s Jimblebar Fines (JMBF) and Mining Area C Fines (MACF), both facing periods of improved sales as demand from the Chinese market centered around cargoes with wider discounts as end-users grappled with mill margin woes.

The generally steady trickle of spot supply of medium-grade fines amid capped demand over the same period created an oversupplied market, applying downward pressure on the Platts IODEX.

Source: Platts