Investing In The Next Steel Bull Market With OM Holdings

Time:Wed, 16 Sep 2020 10:29:51 +0800

keywords :

Introduction

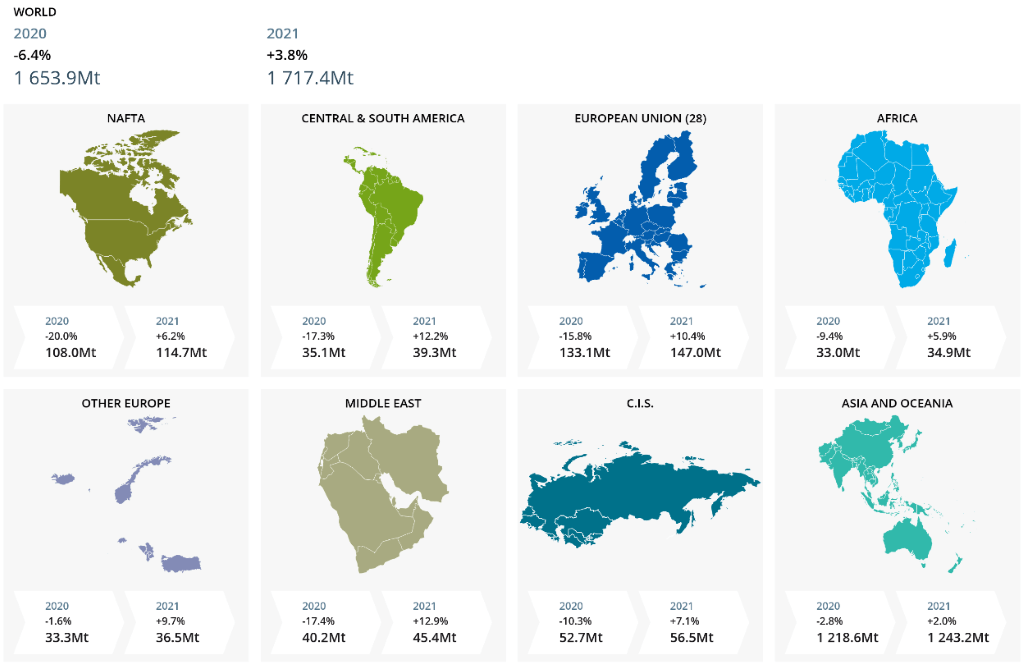

Steel is one of the sectors that has been significantly affected by the COVID-19 pandemic. According to the World Steel Association, global finished steel demand is expected to decline by 6.4% in 2020 and won't be able to recover lost ground in 2021.

(Source: World Steel Association)

However, steel prices are currently near pre-COVID-19 levels as strong demand from China's infrastructure and property sector is driving demand. Still, analysts think Chinese steel demand could start to taper off soon, which would put pressure on prices. Looking at alloys and ores, things are already looking bad, except for iron ore.

(Source: Mint)

The phrase "The cure for low prices is low prices" is popular for commodities, and I think that companies in the steel sector chain with Tier 1 assets that can survive the coming slump will be poised for significant market share gains and share appreciation. One such company in my view is Asia-focused integrated manganese and silicon group OM Holdings (OTC:OMHLF), and I'm surprised no one has covered it yet on Seeking Alpha.

OM's key assets

I've been keeping an eye on the company due to its 13% indirect stake in the Tshipi Borwa manganese mine in South Africa as one of my holdings, Jupiter Mines (OTC:JMXXF), holds a 49.99% interest in the same operation. OM also owns the Bootu Creek manganese ore mine in Australia and also has a marketing and trading arm, which deals in manganese ore, ferrosilicon, silicomanganese, and ferromanganese, among others. However, its main business involves the production of ferrosilicon, silicomanganese, and high-carbon ferromanganese.

(Source: OM Holdings)

The company owns a smelter in southern China, which has a manganese alloy capacity of 80ktpa and a sinter ore capacity of around 300ktpa. Its flagship project is the $500 million Sarawak smelter complex in Malaysia, which is a 75:25 joint venture with Malaysian conglomerate Cahya Mata Sarawak (OTCPK:CHYMF). The facility has a capacity of 200-210k mtpa of FeSi and 250-300k mtpa of manganese alloys with a total 10 ferrosilicon furnaces and six manganese furnaces. It was built in 2014 and pivoted into downstream production of Mn/Si products in 2018.

(Source: OM Holdings)

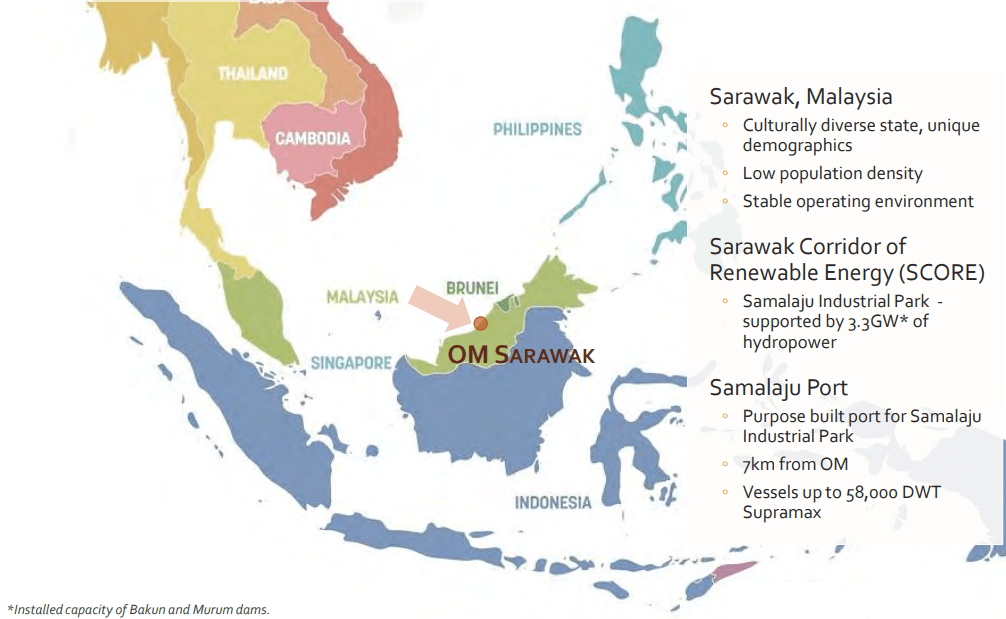

The reason I'm excited about this facility is that the two factors that determine the success of a smelter are present - cheap electricity and location. The Sarawak smelter is located in the Samalaju Industrial Park, which has a purpose-built port and is near several steelmakers. The location is ideal for customers who are uncomfortable in regards to their reliance on China for the supply of ferroalloys.

(Source: OM Holdings)

Looking at electricity supply, smelting is an energy-intensive industry, and sometimes, electricity prices account for nearly half of the cost of production. The Samalaju Industrial Park is powered by the Bakun and Murum dams, and in 2012, OM inked a Power Purchase Agreement (PPA) for a 20-year period with a fixed annual price escalation rate. In 2011, Malaysia's Prime Minister said that the developer of the two dams sold power at 6.25 sen ($0.006) per kW, with a 1.25% annual increase, to Sarawak Energy, which then distributes it to clients.

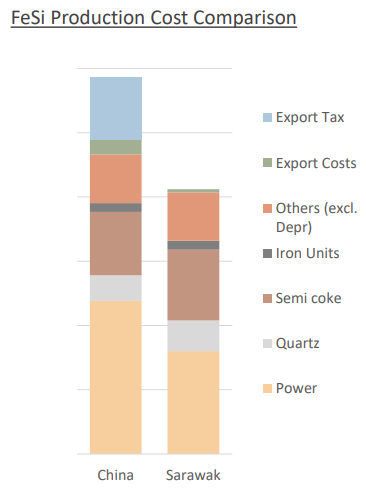

This puts the Sarawak smelter into the first quartile of the global production cost curve and makes it more competitive than Chinese smelters.

(Source: OM Holdings)

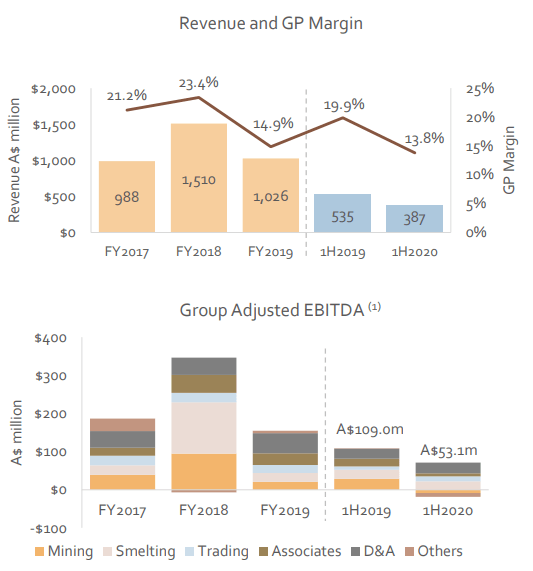

We don't have the exact costs from Sarawak, and the company provides figures for its whole smelting division. However, you can see from the adjusted EBITDA graph of OM that the division can generate EBITDA of around A$140 million ($102 million) during strong years like 2018.

Valuation and main risks

While steel prices are still high, ferrosilicon and manganese ore aren't faring well, and this has put pressure on the finances of many miners and smelters.

(Source: OM Holdings)

While FY18 was a very good year for OM, you can see from the above graph that it was an anomaly and can't be taken as a base case. In the first half of FY20, the company still managed to generate adjusted EBITDA of A$53.1 million ($38.7 million) despite the adverse effects of COVID-19 on its operations. The TTM EBITDA stands at A$98.6 million ($71.8 million).

The net debt is A$410.4 million ($298.9 million), and most of it is related with project financing for Sarawak, meaning they are in Malaysian ringgit. With a market cap A$240.1 million ($174.9 million), the enterprise value stands at A$650.5 million ($473.7 million), and the TTM EV/EBITDA ratio is 6.6 times.

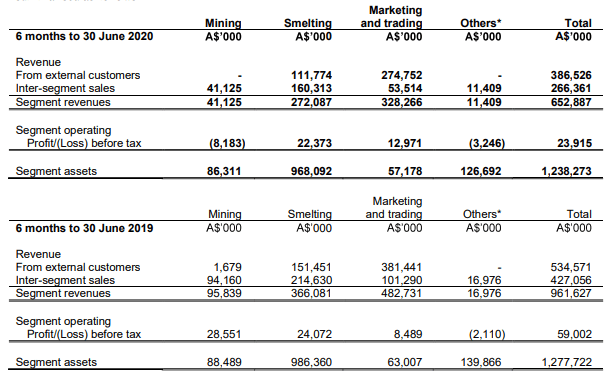

Looking at the profit before tax by segments, you'll notice that most of OM's profit currently comes from its smelting and trading businesses.

(Source: OM Holdings)

Let's be conservative in our valuation and be harsh. The mining business includes the 0.8Mtpa Bootu Creek manganese ore mine, which is riddled with safety issues, and I'm surprised it was allowed to reopen at all. The C1 unit cash operating cost of the mine for the quarter ended June 2020 was $3.06/dmtu, which means that this is not a low-cost operation and will struggle when manganese ore prices are low. In this environment, there doesn't appear to be much value in Bootu Creek.

The stake in Tshipi is accounted for as share of results of associates, and I think we can use the valuation of Jupiter Mines as a starting point. The latter's enterprise value without counting the attributable cash position at Tshipi stands at A$491.3 million at the moment, which means OM's stake in Tshipi could be valued at around A$127.8 million ($93 million). However, Jupiter is also preparing an IPO for its mothballed iron ore assets (I've covered that here), which means the sum should be somewhat lower than that.

Looking at the smelting and trading businesses, we could assign them a multiple of 10 times pre-tax profit and take H1 2020 as a base case. This would value the two businesses at A$706.9 million ($514.8 million), which is around the amount of investment to build Sarawak alone.

Still, combining the valuations of all of OM's businesses minus its net debt is equal to $308.9 million, which gives an upside of over 75% for the company's shares.

Sarawak is a great operation and is generating significant cash flow even in these troubled times. The main risk I see for the bull thesis is a very prolonged period of low manganese ore and ferroalloy prices and a strong Malaysian ringgit. The former could become a reality if steel demand fails to recover fast, and the latter could be a significant headache as OM's debt is in ringgit, and its electricity prices at Sarawak are also in this currency. If operations become unprofitable and debts can't be repaid, the most likely action is a capital increase, which would significantly dilute investors.

Conclusion

Steel and iron ore prices are high but aren't likely to hold, and the ferroalloy and manganese ore markets are already in trouble. With share prices of many smelters and miners at depressed levels, this is a good time to invest in companies with Tier 1 assets as they are most likely to survive and are set to benefit significantly when the market turns. Commodity markets regularly switch between feast and famine, so this is not a new strategy.

I think OM Holdings has a very good smelting operation in Sarawak, which can generate profits even in this challenging market. The company has a relatively high debt level, and I think it would be a good idea to sell the stake in the Tshipi mine to repay some of it. Another prudent thing to do would be to look at a currency hedge.

In any case, OM Holdings looks like a compelling investment opportunity for the long run. Keep in mind that the main listing of the company is on the ASX