Eramet Is Its Own Worst Enemy

Time:Wed, 12 Aug 2020 08:24:28 +0800

keywords :

The company’s Moanda manganese ore mine boosted production just as oversupply in the market was disappearing.

EBITDA fell by 61% in H1 2020, while FCF was negative.

I don’t think there’s much value in any of Eramet's businesses besides the manganese ore unit.

It’s hard to justify a valuation of over $1.1 billion for Moanda at these manganese ore prices.

Introduction

Back in April, I wrote an article in which I forecast that South Africa's nationwide lock-down due to COVID-19 would benefit Gabon-focused manganese ore miner Eramet (OTC:ERMAF; OTCPK:ERMAY) as it would significantly decrease manganese ore stockpiles and fears about a possible shortage would likely to lead to a meaningful increase in manganese ore prices.

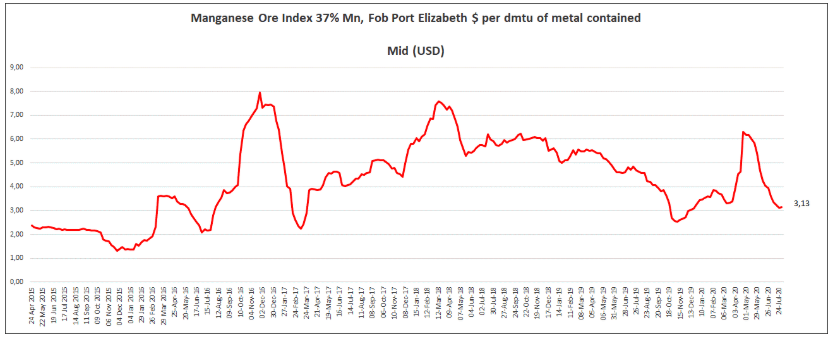

Well, manganese ore prices reached high levels but failed to hold them as the supply gap was plugged by none other than Eramet and the market is once again in oversupply after South Africa reopened.

The manganese ore market in H1 2020

Manganese is an irreplaceable alloy element in steel-making as it improves strength and flexibility. Manganese ore is mainly used in the manufacturing of carbon steel. Production of the latter decreased by 6.1% to 881 Mt during the first half of 2020, mainly due to the impact of COVID-19 on Europe and the USA.

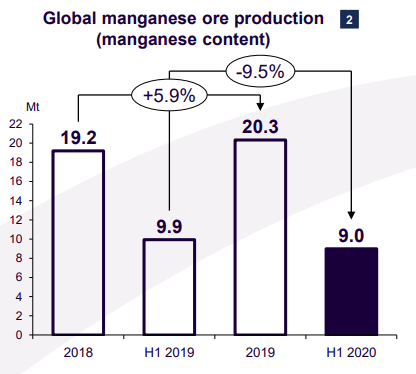

Global manganese ore production, in turn, went down by 9.5% to 9 Mt, but inventories at Chinese ports rose to 5.1 Mt from 4.7 Mt at the end of 2019. This is a very high level, which is equal to around nine weeks of consumption.

Eramet has been operating in Gabon since 1953 through Compagnie minière de l'Ogooué (Comilog), which owns the Moanda manganese ore mine.

The manganese ore market is still in surplus, which can be attributed to Moanda as the latter increased production by 31% on the year to 2.8 Mt during the first half of 2020.

Moanda now accounts for more than 15% of global manganese ore production and I think the latter is the main reason for the 11 consecutive weeks of declines for manganese ore prices. Manganese ore is a bulk commodity and even small surpluses in the market can significantly drive down prices.

With most of Eramet's other businesses under-performing, I think the company would've been in a better financial position if it had decided not to increase Moanda's output.

Eramet's H1 financial performance

Manganese ore currently accounts for around half of Eramet's revenues and almost all of its EBITDA.

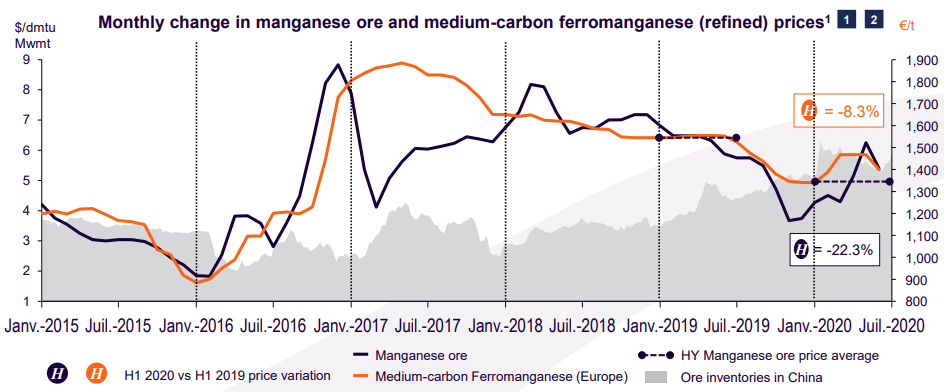

Overall, H1 2020 was horrible for the company as manganese ore and ferronickel prices slumped by 22% and 10% year-on-year. COVID-19 had a significant impact on the company's high-performance alloys division as around a third of orders in the aerospace business were cancelled. I don't expect the situation to improve anytime soon for this division as the International Air Transport Association (IATA) recently projected that global passenger traffic will not return to pre-Covid-19 levels until 2024.

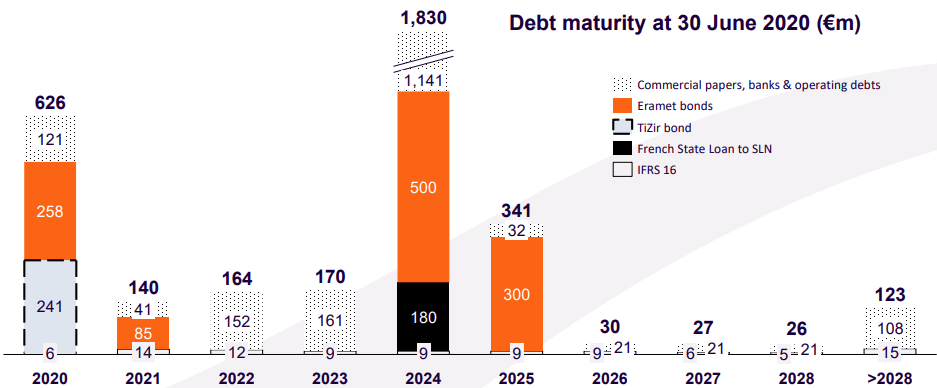

In H1 2020, Eramet had negative free cash flow and net debt increased to 1.54billion euros ($1.75 billion). However, I don't think the company is in danger of insolvency. Eramet will get around $300 million from the sale of its metallurgical conversion plant in Norway and there's no significant debt maturity in the next few years.

Valuation

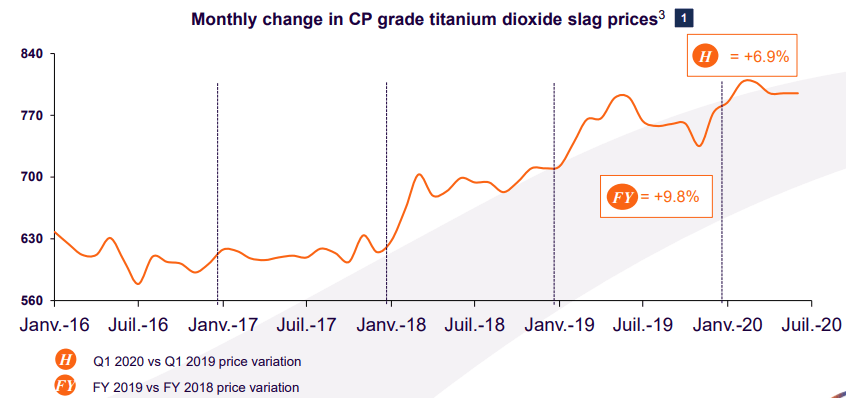

With the global aerospace industry in collapse, I think Eramet's high-performance alloys division will be a drag on results for a long time and the company is better off selling it. The nickel business is also operating at a loss, which is somewhat compensated by the mineral sands division. However, the good performance of the latter can be attributed to high prices of zircon and CP grade titanium dioxide slag. I don't expect these to hold in H2 2020 as both markets are expected to be in oversupply.

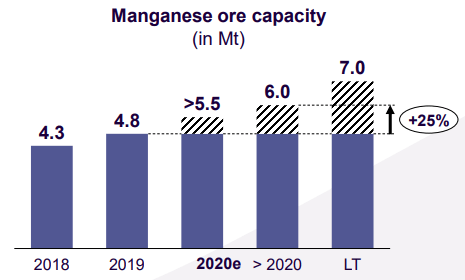

The value of Eramet is in Moanda, which is set to become the largest manganese ore mine in the world with an output of 7 Mt per year. With reserves at 269 Mt, mine life is not an issue.

At the moment, Eramet has an enterprise value of 2.25 billion euros ($2.52 billion), which I find hard to justify. Moanda is a great asset, but I don't see much value in the company's other businesses.

I think a good comparable company for Eramet's manganese business is Africa-focused manganese ore miner Jupiter Mines (OTC:OTC:JMXXF), which owns 49.9% in the 3.6 Mt Tshipi mine in the southern part of the Kalahari Manganese Field in South Africa.

Eramet has three times higher attributable production and is a little ahead on the cost curve, but Jupiter has no debt, distributes all earnings as dividends and the planned IPO of its mothballed iron ore assets will add some value.

Also, both mines are expanding production. While Moanda is targeting 7 Mt per year, Tshipi is on track to be expanded to 4.5 Mt.

At the moment, Jupiter has an enterprise value of A$540.3 million (USD 367.6 million). If we assume Moanda should be valued at around three times higher than Jupiter, this gives Eramet's manganese business a valuation of just over $1.1 billion.

Conclusion

Eramet is in a bad shape due to the impact of COVID-19, with its high-performance alloys business suffering the most.

Moanda is world-class manganese ore mine and has the potential to help Eramet turn FCF-positive and repay debt fast, but is increasing production at the wrong time. With the manganese ore market in oversupply, I think Eramet would be better off keeping Moanda's output at around 5 Mt per year. This would keep the market close to balance and allow manganese ore prices to recover.

Looking at Eramet's valuation, I don't think there's much value in any of its businesses besides the manganese ore unit. Comparing the latter to Jupiter, it's hard to justify a valuation of beyond $1.1 billion. I'm avoiding Eramet for the time being.